When landlords realize they have undeclared rental income, the first question they ask is usually: “How many years of back-tax am I going to have to pay?” There is a common misconception that HMRC can only look back at the last few years. In reality, the “statute of limitations” for Tax Look-back is flexible. In 2026, under the Let Property Campaign (LPC), the length of your “look-back” period depends entirely on your behaviour. HMRC categorizes your actions into three buckets: Reasonable Care, Careless, and Deliberate.

At VA Acounting Solution , we specialize in analyzing your history to ensure you only pay for the years legally required. Here is a breakdown of the 4, 6, and 20-year rules.

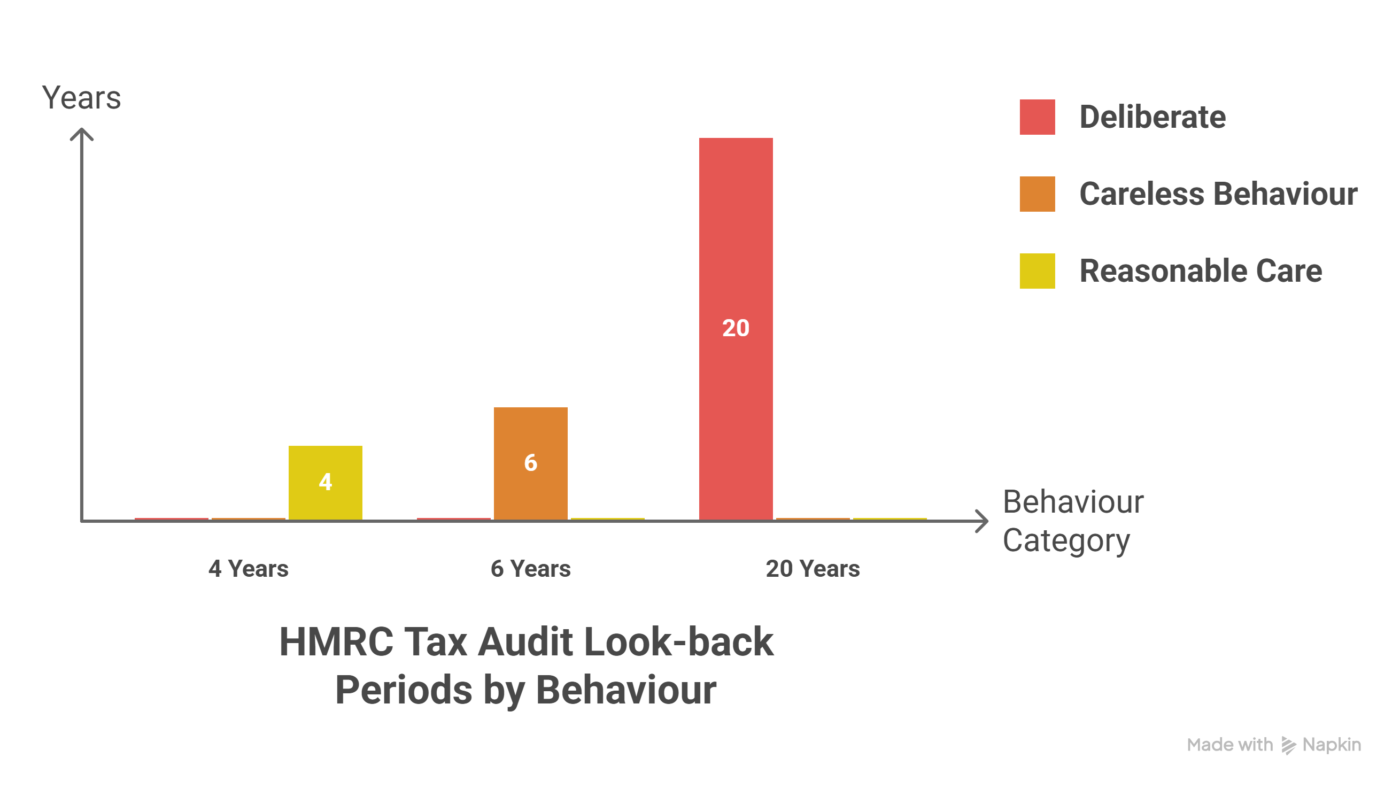

1. The 4-Year Rule: “Reasonable Care”

If you can prove that you took reasonable care but still made a mistake, HMRC is limited to looking back only 4 years.

What defines “Reasonable Care”?

HMRC acknowledges that tax is complicated. You might fall into this category if:

- You sought advice from a professional that turned out to be incorrect.

- You made an honest mathematical error despite keeping good records.

- You reasonably believed you didn’t owe tax (e.g., your expenses legitimately wiped out your profit, but you didn’t realize you still had to file a nil return).

The Result: You pay the tax and interest for the last 4 years, and often, you can negotiate a 0% penalty.

2. The 6-Year Rule: “Careless” Behaviour

The most common category for “accidental landlords” is Careless Behaviour. This applies if you failed to tell HMRC about your rental income because you didn’t check the rules, but you weren’t trying to hide the money.

Examples of Careless Behaviour:

- You moved in with a partner and rented your old flat but “forgot” to tell HMRC.

- You assumed your letting agent was paying your tax for you.

- You didn’t keep proper records and guessed your figures.

The Result: HMRC can go back 6 years. Penalties for an unprompted disclosure in this category typically range from 0% to 30%.

3. The 20-Year Rule: “Deliberate” or “Failure to Notify”

This is the most serious category. If HMRC believes you knew you had a tax obligation and chose to ignore it, or if you failed to notify them that you had started a rental business, they can go back 20 years.

What defines “Deliberate” Behaviour?

- You intentionally kept rental income out of your tax returns to pay less tax.

- You provided false information to HMRC or concealed records.

- You have been a landlord for a decade but never registered for Self Assessment.

The Result: You must disclose every year of income for the last two decades. Penalties for deliberate acts are much higher, ranging from 20% to 100% (and up to 200% if the income involves offshore accounts).

4. The “Offshore” Exception: The 12-Year Rule

In 2026, there is a specific mid-tier rule for landlords who live abroad or have overseas rental property. If an error involves offshore income or gains, and it was “Careless” or even if “Reasonable Care” was taken, HMRC has a standard look-back period of 12 years. The only way to stick to 4 or 6 years in an offshore context is to prove a very specific “reasonable excuse.”

5. How Behaviour Impacts Your Penalty (The “Felix” Strategy)

At VA Accounting Solution, our job is to act as your advocate. HMRC will often start by assuming a landlord was “Deliberate” to maximize the tax collected. We counter this by:

- Evidence-Based Arguments: We present your “Reasonable Excuse” (e.g., serious illness, bereavement, or reliance on a trusted family member) to move you from the 20-year bracket to the 6 or 4-year bracket.

- Proactive Disclosure: By using the Let Property Campaign voluntarily, we demonstrate that you are not “concealing” income, which is the strongest defense against the 20-year rule.

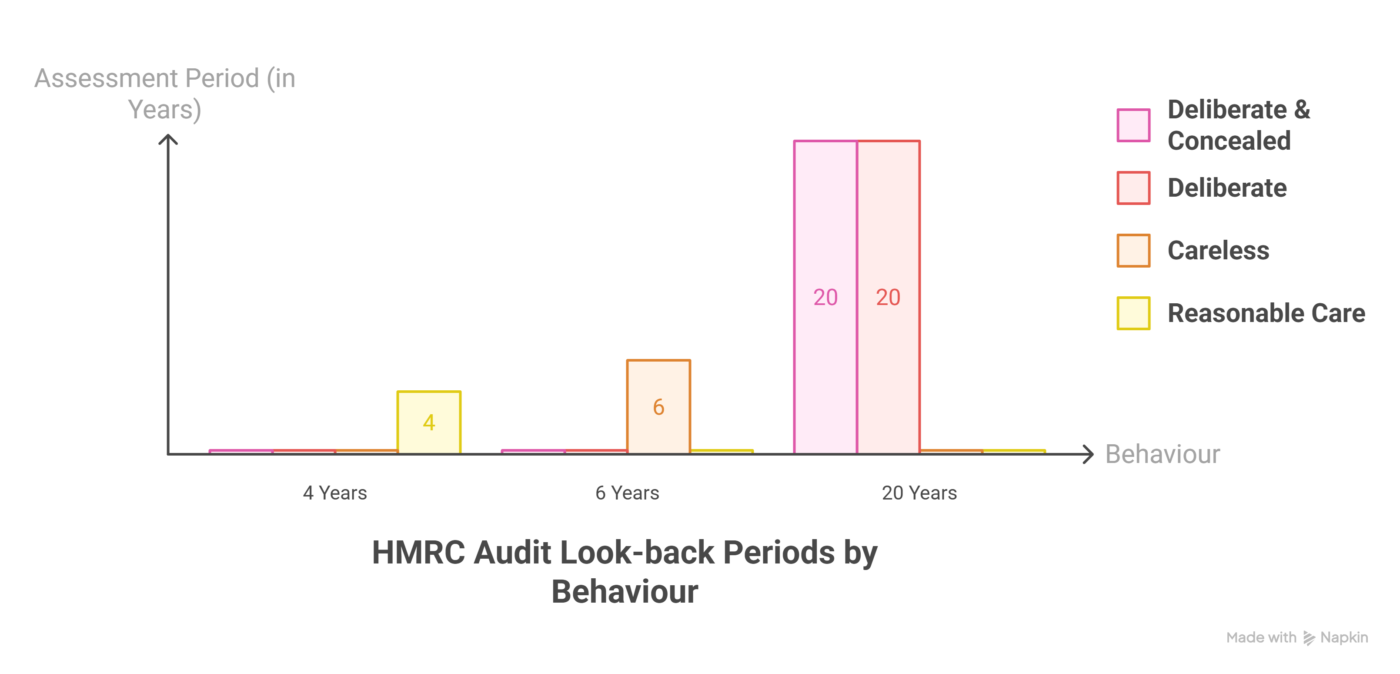

| Behaviour | Assessment Period | Penalty (Unprompted) |

| Reasonable Care | 4 Years | 0% |

| Careless | 6 Years | 0% – 30% |

| Deliberate | 20 Years | 20% – 70% |

| Deliberate & Concealed | 20 Years | 30% – 100% |

6. Can HMRC Find Me After 20 Years?

Many landlords think, “I’ve been doing this for 15 years and haven’t been caught yet; surely I’m safe?” In the digital age, the answer is no. HMRC’s Connect system has a “long memory.” When you eventually sell the property, the Land Registry data from 20 years ago will be cross-referenced with your tax history. If there’s a 20-year gap where you owned a second property but paid no tax, an investigation is highly likely at the point of sale.

Frequently Asked Questions (FAQs)

Q1: What if my rental business made a loss 5 years ago?

If you made a legitimate tax loss in a specific year (e.g., due to major repairs), that year does not “count” toward your liability, though it still falls within the look-back window. We can often use those losses to offset profits in later years.

Q2: My father died and left me a rental property he never declared. How many years do I pay?

For deceased estates, the rules are slightly different. Usually, HMRC is limited to looking back 6 years prior to the date of death, provided the executors settle the matter promptly.

Q3: Does the 20-year rule apply if I simply didn’t know the law?

HMRC generally argues that “ignorance of the law is no excuse.” However, if we can show you had a “Reasonable Excuse” for not knowing (such as being given bad advice by a previous accountant), we can often fight to keep the period to 6 years.

Q4: If I come forward now, can I choose which years to pay?

No. An LPC disclosure must be “full and complete.” You cannot “cherry-pick” years. If you disclose 5 years but HMRC finds you’ve been a landlord for 15, they will reject your disclosure and open a fraud investigation.

Q5: Will HMRC ask for bank statements from 20 years ago?

If you are in the 20-year bracket and don’t have records, we use “Reasonable Estimations.” We can use historic rental averages and ONS data to recreate your accounts in a way that HMRC will accept.

Know Your Years, Protect Your Future

Determining your “behaviour” is the most technical part of a tax disclosure. Don’t guess and end up paying for 20 years when you only owed 6.

Contact VA Accountants Solution today. We will review your history and ensure your disclosure is handled with the correct look-back period.